A significant improvement in market risk sentiment weighed on the US dollar against just about every other currency in the world on Tuesday, while leading to rallies in equities and a sell-off in government bond markets.

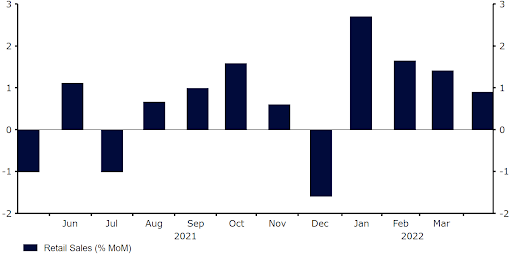

Tuesday’s US retail sales figures also provided reason for optimism that rampant inflation is not yet having a material impact on consumer spending activity. Headline US retail sales increased by a larger-than-expected 0.9% month-on-month in April (0.7% expected), with the March data also revised sharply higher (+1.4% vs. +0.5%). While the strength of the data would ordinarily be viewed as a US dollar positive, we see it as a further indication that consumer spending is holding up well in the face of aggressive price increase – a good sign for global growth and risk assets.

Figure 1: US Retail Sales (2021 – 2022)

Among the major currency pairs, EUR/USD has advanced back above the 1.05 level, with talk of parity in the pair dying down for now. The common currency was further supported by some hawkish comments from ECB member Knot, regarded by many as the most hawkish member on the Governing Council. Speaking yesterday, Knot said that a 50 basis point rate increase cannot be ruled out when the ECB meets in July should data show that inflation was broadening. While we see this as an extreme view, it is clearly a sign that the bank is well on the way to beginning its hiking cycle, with a 25 basis point move in July seemingly a done deal.

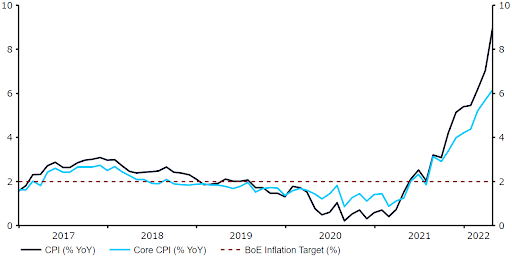

Sterling has also rebounded off its lows, briefly touching the 1.25 level against the US dollar on Tuesday. The UK currency was supported by yesterday’s strong employment data, which showed a move lower in unemployment (3.7% from 3.8%), and an increase in wages (up to 7% in the three months to March including bonuses, from 5.6%). That said, we’ve seen a little bit of a sell-off in the pound following this morning’s UK inflation data, which slightly missed expectations. Inflation rose to a 40-year high 9.0% last month (9.1% expected), with the alarming increase in prices driven largely by jumps in electricity (up 53%) and gas (up 95%).

Figure 2: UK Inflation Rate (2017 – 2022)

The Bank of England is stuck between a rock and a hard place, as it aims to balance reining in the surge in prices, with supporting the fragile growth outlook. Unfortunately, the situation is likely to get worse, before it gets better, with the MPC expecting inflation to peak in excess of 10% in the coming months. While much of the increase in prices is driven by factors out of the bank’s control, such as rising commodity prices, we think that further rate hikes are inevitable. Indeed, we will be looking for the bank to shift away from its recent dovish rhetoric at its next meeting in June, and open the door to a continuation of its recent aggressive pace of hikes through year-end.

To stay up to date with our publications, please choose one of the below:

📩 Click here to receive the latest market updates

👉 Our LinkedIn page for the latest news

✍️ Our Blog page for other FX market reports